Post #002 : Country Deep Dive - Greece

Fourteen months before MSCI formally moves it to developed markets, here is the honest case for and against the trade.

There are second acts in markets, just as there are in life. They are rarer than people think, harder to execute than they appear, and the investors who profit from them are almost never the ones who arrive after the story is already on the front page.

Greece may be one of the more extraordinary second acts of the past decade. Or it may be a very old story dressed up in new clothes. The MSCI announcement came yesterday - March 31, 2026. The question of which interpretation is correct will determine whether the next 14 months are rewarding or instructive.

A Brief History of Humiliation

To understand why anyone finds Greece interesting in 2026, you need to remember what it looked like in 2015.

Capital controls. Bank closures. ATM queues around the block. A stock market that physically shut for weeks. When it reopened, bank shares had fallen 94%. The Athens exchange became smaller than Egypt’s and Morocco’s by market capitalisation. The debt ratio breached 180%. Three consecutive bailouts totalling €289 billion. Unemployment hit 28%.

Greece had been a founding member of the MSCI Emerging Markets Index in 1988, upgraded to developed market status in 2001, then downgraded back to emerging markets in 2013 as the crisis made it functionally uninvestable for international institutions.

That is the ghost. It still lives in the mental models of many allocators who watched it happen and drew their conclusions. Today, MSCI announced Greece will be reclassified back to developed market status - effective May 2027. It has come full circle.

The question is whether the trade has too.

What Greece Actually Is Today

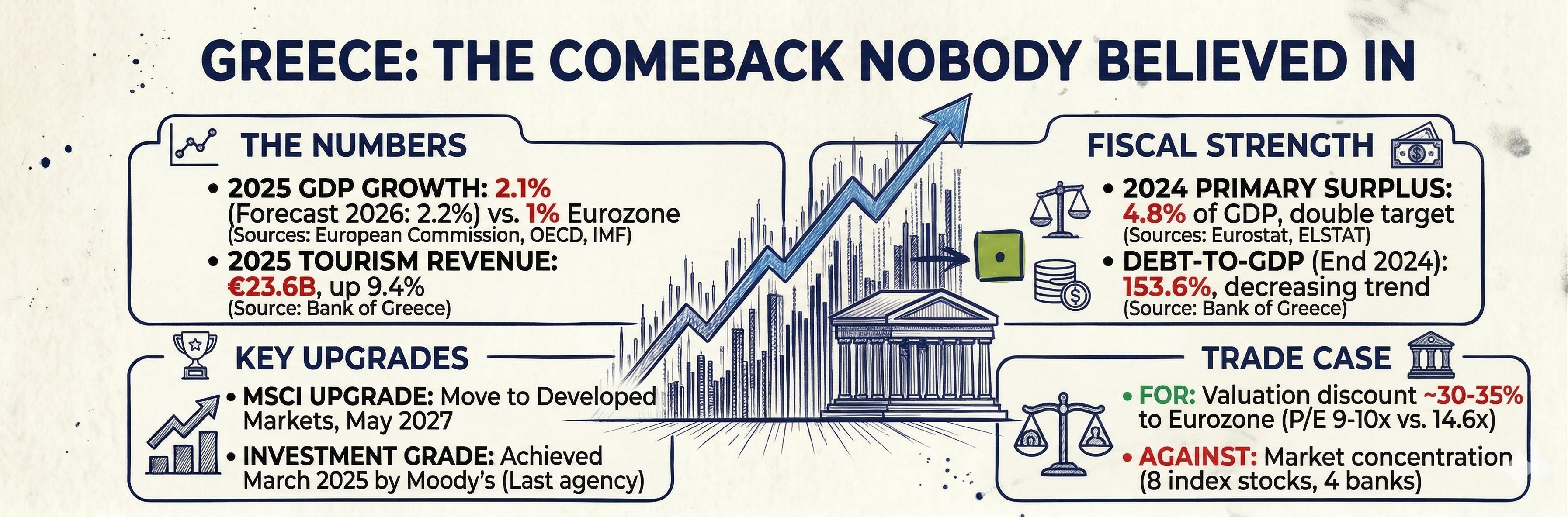

Greece is the 50th largest economy in the world by nominal GDP at $282 billion, the 16th largest in the EU. GDP per capita is $27,170 - comfortably within developed economy territory by any standard measure. (IMF, 2025)

Growth was 2.1% in 2025 and is forecast at 2.2% in 2026, both well above the eurozone average of approximately 1%. Greece has outpaced the eurozone consistently since 2021. Tourism revenues hit a record €23.6 billion in 2025, up 9.4%, with arrivals growing 5.6% to nearly 38 million - the third consecutive record year. (Bank of Greece, February 2026)

Greece posted a primary surplus of 4.8% of GDP in 2024, confirmed by Eurostat and ELSTAT - nearly double its own target, and one of only six EU countries to post any surplus at all that year. Debt at end 2024 stood at 153.6% of GDP, down from a peak above 200%, projected to fall below 140% by 2027. Still the highest in Europe, but declining at one of the fastest rates anywhere. (European Commission; Bank of Greece)

Moody’s upgraded Greece to investment grade in March 2025 - the last major rating agency to do so, ending fifteen years of sub-investment-grade status. That single event quietly reopened the Greek government bond market to a large category of institutional investors who had been mandatorily excluded for over a decade.

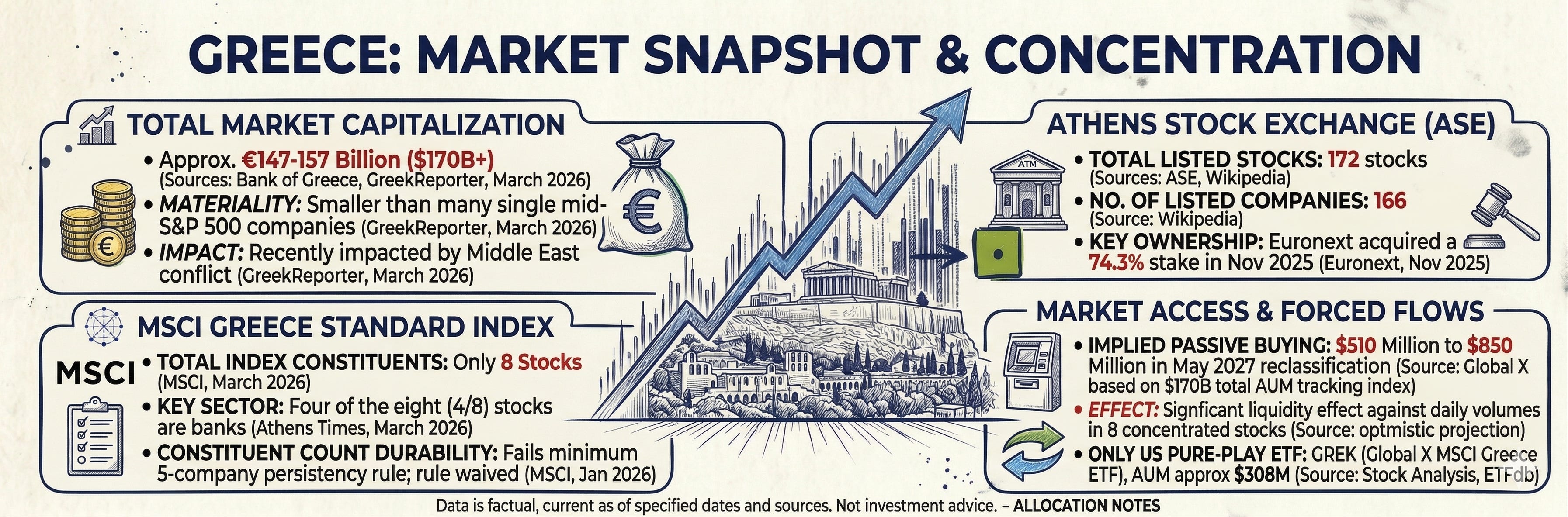

The stock market is small. The Athens exchange lists 172 stocks across 166 companies. Total market capitalisation sits at approximately €147 to 157 billion — smaller than a single mid-large cap company in the S&P 500. In November 2025, Euronext acquired a 74.3% controlling stake in the Athens exchange, placing Greek equities inside the same infrastructure as Paris, Amsterdam, Brussels, and Lisbon. The plumbing of market integration tends to precede the capital flows that follow.

The MSCI Greece Standard Index has eight constituents: OTE in telecom, OPAP in gaming, Jumbo in retail, PPC in power, and four banks — Eurobank, Alpha Bank, Piraeus, and National Bank of Greece. Four of eight stocks are banks. This is the central risk of the entire investment case.

Valuation is genuinely interesting. MSCI Greece trades at approximately 9 to 10x forward earnings. MSCI Europe trades at 14.6x. A 30 to 35% discount, for an economy growing at double the European pace. Either the market is mispricing something, or the discount is there for reasons that will persist. (Global X ETFs research, July 2025)

How Greece Actually Turned It Around

The fiscal turnaround was not achieved through austerity alone. The more interesting story is what happened after the cuts.

The single most consequential reform was the digitalisation of tax enforcement. Greece’s shadow economy was estimated at approximately 27% of GDP at the peak of the crisis - one of the highest ratios in Europe. An IMF study estimated that 75% of self-employed professionals declared income below the taxable threshold. The government was collecting far less than the economy was actually generating. (IMF Finance & Development, 2019)

Greece built an independent tax authority - AADE - insulated from the political interference that had made enforcement a joke for decades. It introduced mandatory card payment acceptance, e-invoicing, real-time reporting, and a digital labour card that formalised previously undeclared employment. Electronic payments for childcare services alone rose 433% in 2024. Tax revenues from anti-evasion efforts increased by approximately 3% of GDP. That is not growth. That is the same economy being measured honestly for the first time. (IMF Finance & Development, Hatzidakis, 2025; Invezz, April 2025)

Moody’s cited this digital transformation specifically in its March 2025 upgrade, calling it durable institutional change rather than cyclical improvement. Finance Minister Kyriakos Pierrakakis has described it as irreversible. Once transactions are digital, they cannot easily become invisible again.

The banks were repaired in parallel. Non-performing loan ratios dropped to approximately 3% through the Hercules Asset Protection Scheme and sustained recapitalisation. The four systemically important banks are now generating profits, not requiring survival support. (IMF Article IV 2025)

One honest qualification. The surplus has been described by opposition parties as a blood-stained surplus - VAT at 24% remains among the highest in Europe, and real wages are still approximately 30% below 2009 levels. Growth has been real. Its distribution has not been equitable. For the investor, what matters is whether the institutional framework is durable. The evidence suggests it is, precisely because it is digital and structural rather than political and reversible.

The Rule MSCI Bent to Make This Happen

Greece did not actually meet MSCI’s standard criteria for reclassification. It failed the size and liquidity persistency rule, which requires a minimum of five companies meeting developed market criteria over each of the last eight index reviews. With only eight constituents in total, meeting this rule consistently is structurally difficult.

MSCI waived the rule. Institutional investors argued that treating Greece differently from other EU members was inconsistent with the degree of economic and financial integration across the bloc. EU membership itself, they said, is the developed market credential — harmonised regulation, common currency, integrated clearing infrastructure. MSCI agreed. (MSCI press release, March 31 2026; Markets Media, January 2026)

This matters for two reasons. It tells you how the global investment community thinks about EU integration as an investment framework. And it raises a quiet question: if the rule was waived once, it can be waived again. For most investors this is a footnote. For those who think carefully about index methodology, it is worth a note in the margin.

What Israel Taught Us

The closest precedent is Israel, upgraded from emerging to developed market by MSCI in May 2010. Before the upgrade, Israel represented approximately 3% of MSCI EM - a meaningful weight that attracted dedicated fund flows. After the upgrade, it became 0.4% of MSCI World. A significant fish in a small pond became a tiny fish in a large ocean. The forced buying from developed market trackers did not offset the forced selling from EM managers who had to exit. The net result was a decrease in foreign fund involvement in Israeli equities. (Start-Up Nation Policy Institute; VanEck Israel commentary)

Greece currently represents less than 0.7% of MSCI EM - already tiny. The forced EM selling will be modest. Greece enters MSCI Europe, tracked by funds managing well over $170 billion.

At 0.3 to 0.5% of MSCI Europe, the implied passive buying is $510 million to $850 million arriving on a known date in May 2027. Against daily Athens trading volumes in eight concentrated stocks, that is material. Against total market cap of $170 billion, it is not transformational. The dynamic here is better than Israel’s - Greece enters MSCI Europe directly rather than a less-tracked regional index. But the basic reality of becoming a small weight in a very large index still applies.

The Honest Investment Case

Three things work for Greece. Three work against it.

For: The valuation gap is real. At 9 to 10x forward earnings versus Europe at 14.6x, with GDP growing at double the European pace, the case for multiple expansion over three to five years is coherent — if the fundamental story holds. The catalyst is real and dated - passive managers must buy by May 2027. And EU Recovery funds continue to support investment through 2026, with fixed capital investment growing 8.9% in full-year 2025.

Against: Concentration is the defining risk. Eight stocks, four banks. Buying Greece means making a deliberate call on Greek banking profitability and domestic credit growth. Fine to do consciously. Dangerous to do by accident. Liquidity at institutional scale is also a real constraint — GREK, the only pure-play Greece ETF in the US, manages approximately $308 million. An institution deploying $500 million will move prices against itself.

The Middle East conflict is a direct threat. Greece is a net energy importer — every $10 rise in oil reduces GDP by approximately 0.15%. Tourism is the economy’s primary growth engine, and the Athens market has already shed approximately €10 billion in market cap since hostilities began. (GreekReporter, March 2026; Optima Research)

And the most uncomfortable question: how much is already priced in? The Athens index is up nearly 35.9%, and MSCI Greece is up 37.8% over the past twelve months (USD %, as of 31 March 2026). MSCI’s announcement was widely anticipated - the consultation ran from January to March. The investor who bought Greece two years ago has already made the money.

How to Access the Trade

GREK (Global X MSCI Greece ETF) is the only pure-play Greece ETF in the US -approximately 15 stocks, heavily weighted toward financials, AUM around $308 million. The most direct route to the upgrade catalyst. Notably, GREK continued trading in New York when the Athens exchange physically closed during the 2015 capital controls crisis.

Direct Athens exchange access allows more precision. The eight MSCI constituents are the most liquid - OTE, Eurobank, National Bank of Greece, and Alpha Bank draw the most institutional volume.

Greek government bonds are now investment grade at every major agency. Yields sit broadly in line with other peripheral European sovereigns — slightly above Spain, below Italy and France. (Morningstar DBRS, September 2025)

European equity funds with Greece exposure offer diluted access within a diversified wrapper - suitable for mandates that cannot take single-country concentration.

The Lesson

Greece in 2026 is not the same country as Greece in 2015. The digital tax enforcement is structural, not cyclical. NPLs at 3%, banks profitable, tourism at three consecutive records, investment grade at every major agency, debt declining at one of the fastest rates in Europe.

But markets price stories on a lag in both directions. Greece was priced for permanent catastrophe long after the catastrophe had passed. Whether it is now priced for optimism that has run ahead of the fundamentals is the honest question.

The MSCI upgrade is a milestone, not a catalyst. It confirms something the data has been saying for three years. The investors who acted on that data three years ago already know how this chapter ends.

The investors reading about it today are starting a different chapter. The returns will be determined not by today’s announcement, but by whether Greek banks keep healing, tourists keep coming, and the post-RRF economy can sustain momentum without its scaffolding.

A country that went from developed to emerging and back to developed in twenty-six years is either proof of extraordinary institutional resilience, or a reminder that classifications are lagging indicators dressed up as forward signals.

The honest answer is probably both.

Sources: MSCI press release and consultation documents, January to March 2026; IMF Article IV Consultation on Greece, 2025; IMF Finance & Development, Hatzidakis, 2025; European Commission Economic Forecast, Autumn 2025; OECD Economic Outlook, December 2025; Bank of Greece, February 2026; Eurostat/ELSTAT, April 2025; IMF World Economic Outlook, 2025; Athens Stock Exchange; Euronext, November 2025; Global X ETFs, July 2025; ETF.com, August 2025; Start-Up Nation Policy Institute; VanEck Israel; GreekReporter, March 2026; Athens Times, March 2026; Moody’s, March 2025; Morningstar DBRS, September 2025; Press Democrat, September 2025; Invezz, April 2025; Trading Economics; Optima Research.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice, a solicitation, or a recommendation to buy or sell any security. All data is sourced from publicly available information and believed to be accurate as of the date of publication but may be subject to change. The author may or may not hold positions in instruments mentioned. Past performance is not indicative of future results. Always conduct your own research or consult a qualified financial advisor before making investment decisions. Nothing in this publication creates a fiduciary relationship between the author and the reader.