Post #004 : 1,700 Stocks, Three Factors, One Bet on the World Outside America

The investors quietly moving away from US dominance are not being contrarian. They are being careful. Here is the product many of them are using — and whether it deserves the attention it is getting.

Something has shifted in how serious investors talk about the United States.

It is not a sudden thing. It has been building through tariff escalations, debt ceiling brinkmanship, a Federal Reserve whose independence feels less guaranteed than it once did, and a broader unease about whether the institutional architecture that made US assets the default safe harbour for global capital — Pax Americana, in shorthand — is as durable as a decade of S&P 500 outperformance suggested.

The numbers are starting to reflect it. The dollar has weakened. US equity multiples, already stretched by historical standards, are being questioned in a way they were not twelve months ago. European defence spending is accelerating. Japanese corporate governance reform is delivering results. And for the first time in years, international equities are meaningfully outperforming their US counterparts.

I have been looking at this shift from the product side — specifically, which investment vehicles give you genuine exposure to the world outside the US without simply swapping one concentration risk for another. Single-country ETFs are too specific. Broad international trackers give you too much dilution and too little factor discipline. What you want is something that casts a wide net geographically but applies a rigorous filter for quality.

AVDV is an interesting answer I have found to that specific question. It is not a perfect answer — no fund is — but the construction is serious, the team behind it is exceptional, and the current regime may be precisely the environment it was built for.

Whether that bet pays off depends less on the fund itself, which is well-constructed by any reasonable measure, and more on whether the macro conditions supporting it persist. The fund is the tool. The regime is the question.

What AVDV Is

The Avantis International Small Cap Value ETF launched on September 24, 2019, managed by Avantis Investors, a subsidiary of American Century Investments. AUM stands at approximately $17.4 billion as of March 2026. The expense ratio is 0.36%. (Dividend.com, March 2026)

The fund invests in non-US small-cap value companies across developed markets. It does not track an index — it is actively managed, with a benchmark of the MSCI World ex-US Small Cap Index that it aims to beat rather than replicate. Over its lifetime it has largely succeeded: since inception the annualised return is 14.1% (as of 31st Mar’26, in USD terms) , against the benchmark’s considerably lower figure. In 2025, the total return including dividends was 49.4% in USD terms. (Bloomberg)

The DFA Connection

The four founding portfolio managers — Eduardo Repetto, Mitchell Firestein, Ted Randall, and Daniel Ong — all came from Dimensional Fund Advisors. Repetto served as Co-CEO and Co-CIO of DFA until 2017. Firestein and Randall were DFA portfolio managers for US and international strategies. Ong spent over a decade as a DFA senior portfolio manager managing international and emerging markets equity strategies. (MutualFunds.com)

This lineage matters because it explains the investment philosophy. DFA was one of the firms that built the empirical case for factor investing — the idea that small-cap stocks, value stocks, and profitable companies have historically delivered excess returns above the broad market over long time horizons, with theoretical foundations in the Fama-French research. AVDV is essentially DFA’s approach with more active discretion and in some respects lower cost.

The key departure from pure passive factor investing is that Avantis gives its managers discretion to consider implementation costs, tax consequences, and trading timing. The fund does not mechanically rebalance on a fixed schedule the way a passive factor ETF would. Instead it manages factor exposures continuously, adjusting positions when it can do so efficiently. This is a meaningful distinction — it means the fund is not forced to buy stocks that have just become cheap or sell stocks that have just become expensive simply because an index reconstitution demands it.

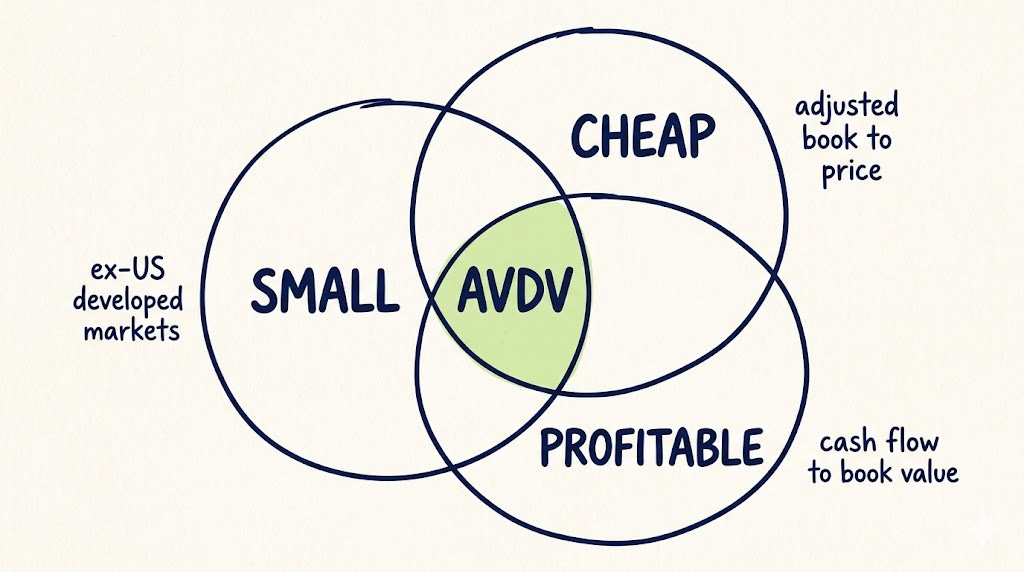

The Investment Process: Three Factors, Actively Applied

The most immediately striking number in the AVDV portfolio is the holding count. At any given point the fund holds between 1,600 and 1,700 individual securities. The top ten holdings account for just 8.2% of total assets. The top holding — Mitsui Kinzoku Company, a Japanese metals manufacturer — is approximately 1.4% of the fund. (StockAnalysis, StockAnalysis holdings data)

This extreme diversification is intentional and has a specific logic. In small-cap markets, individual stock risk is high. Companies are less covered by analysts, less liquid, more volatile, and more exposed to idiosyncratic events. A single bad holding in a concentrated portfolio can cause meaningful damage. By owning 1,700 companies, AVDV essentially eliminates individual stock risk almost entirely. What remains is pure factor exposure — the systematic return from owning small, cheap, profitable companies as a class, rather than any specific company’s fortunes.

The practical implication is important for investors to understand. You are not buying AVDV because you have a view on Mitsui Kinzoku or OceanaGold or Whitehaven Coal, the current top holdings. You are buying a factor — a bet that the broad category of non-US small-cap companies that score well on value and profitability metrics will, on average, outperform the broader international market over time. The individual names are largely irrelevant. The factor exposure is everything.

This has clear benefits: genuine diversification, low individual stock concentration risk, and a clean expression of the underlying investment thesis. The portfolio turnover rate of just 4% against a category average of 44% confirms the fund is not actively trading ideas but maintaining factor exposures efficiently over time. (AAII ETF Evaluator)

The downside is equally clear. When the factors are out of favour — when investors pay up for growth, momentum, or quality rather than value; when small caps underperform large caps; when international markets lag the US — AVDV will struggle. It has no stock-picking edge to fall back on when the factor tailwind disappears. This is not a criticism of the fund so much as a description of what it is. Factor investing requires patience that is frequently uncomfortable.

The Current Portfolio: What 1,700 Stocks Actually Look Like

Despite the breadth, the portfolio has a distinct character that reflects current factor exposure.

The top holdings are heavily weighted toward gold miners and commodity producers — OceanaGold, New Gold, Regis Resources, B2Gold, Perseus Mining all feature prominently alongside Mitsui Kinzoku. (Yahoo Finance holdings data) This is not a deliberate sector call by the managers. It is the output of the factor screens: gold miners and commodity producers in international developed markets are currently cheap on book-to-price ratios and generating strong operational cash flows relative to their asset bases. The factor model is identifying them as small, cheap, and profitable. Whether you find that reassuring or concerning depends on your view of commodity prices.

Geographically, Japan is the largest country allocation, consistent with the fund’s history of overweighting Japanese small caps. Japan’s corporate governance reforms have improved return on equity across its corporate sector, and Japanese small caps have been among the most attractive value opportunities in developed markets for several years. (ETF Trends, January 2026) Europe — UK, Germany, France — provides substantial additional weight. Australia contributes meaningfully, partly via the commodity producers.

The sector breakdown tilts heavily toward industrials, materials, and financials. Consumer staples, technology, and healthcare are underweighted relative to the broad market. This is the natural output of value screens applied to small caps: cyclical, asset-heavy businesses tend to be cheap, while defensive growth companies and technology firms tend to be expensive.

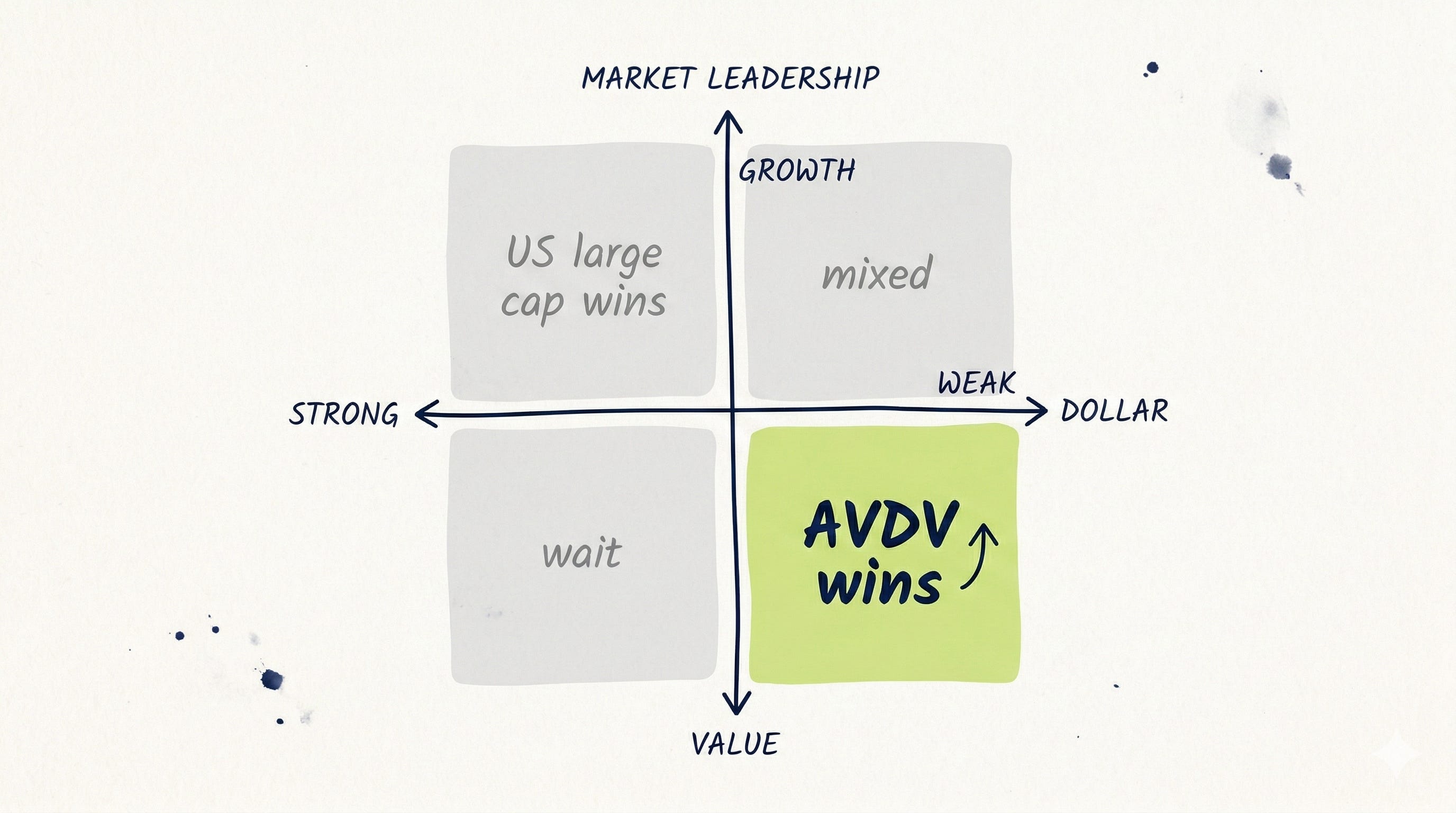

The Current Regime: Why This Matters Now

AVDV has attracted $5.5 billion in net inflows over the past year and $1.3 billion in the most recent quarter alone. (ETFdb.com) That is not passive allocation drift. That is active positioning. Understanding why requires understanding what has changed.

Three things are working for AVDV in the current environment.

The first is dollar weakness. AVDV is unhedged — its returns to US investors include both the underlying equity return and the currency effect. A weakening US dollar amplifies returns from international holdings when translated back into dollars. The dollar has been under pressure in 2026 as the Fed holds rates while other central banks remain more hawkish, compressing the interest rate differential that had supported dollar strength. (Seeking Alpha, January 2026)

The second is valuation divergence. US large-cap equities, particularly the mega-cap technology names, are trading at historically elevated multiples. AVDV’s portfolio trades at a significant discount — a natural consequence of its value screen. When investors begin to question whether US large-cap multiples are sustainable, the relative cheapness of international small-cap value becomes more compelling as an alternative.

The third is the international equity cycle. 2025 saw international equities broadly outperform US equities for the first time in several years, driven by European fiscal expansion, Japanese corporate reform, and a rotation away from US concentration risk.

The Honest Risks

Three risks deserve direct attention.

Factor timing is the most fundamental. The value premium is real over long time horizons. It is not reliable over short or medium ones. There have been extended periods — the late 1990s technology boom being the clearest example — where value strategies significantly underperformed growth for years at a time. An investor in AVDV needs to accept that the fund may lag for extended periods without this representing a failure of the strategy.

Currency risk is the most immediate. An unhedged international fund is a leveraged bet on dollar weakness. If the dollar strengthens — due to a Fed pivot, a flight to safety in a global risk-off event, or simply a reversal of recent trends — AVDV’s returns in dollar terms will suffer even if the underlying equity portfolio performs well. For US investors, this is worth understanding explicitly before allocating.

Commodity concentration is the most overlooked. The current top holdings — gold miners, copper producers, coal companies — reflect the output of a value screen in a specific market environment. These are not permanent fixtures. But they are there now, and they introduce commodity price sensitivity that is not always obvious from the fund’s label as an international small-cap value ETF. A correction in gold or base metals would likely register in AVDV before it registered in most international equity benchmarks.

The Bottom Line

AVDV is the right fund for a specific kind of investor: one with genuine conviction in factor investing, a long time horizon measured in years rather than quarters, tolerance for the periods when factors are out of fashion, and a view that the current environment — weakening dollar, elevated US valuations, improving international earnings — supports the thesis.

It is not the right fund for an investor who wants to track international equity markets broadly, or who has a concentrated view on specific countries or sectors, or who cannot stomach watching a fund underperform during a US large-cap growth rally.

The team is exceptional. The process is rigorous. The cost is fair. Whether the next chapter rewards the thesis depends not on the fund but on the market cycle — and on whether the shift away from US large-cap dominance is a genuine regime change or another head fake.

History says factor premia are real. History also says patience is the price of admission.

Sources: Dividend.com AVDV profile, March 2026; StockAnalysis AVDV data; AAII ETF Evaluator, AVDV; MutualFunds.com AVDV profile; ETFdb.com AVDV fund flows; Yahoo Finance AVDV holdings; Morningstar AVDV analyst rating, June 2025; ETF Trends, Japan international equity analysis, January 2026; Seeking Alpha, AVDV 2026 outlook, January 2026; Tickeron AVDV analysis; ETF Trends, AVDV December 2025 outlook.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice, a solicitation, or a recommendation to buy or sell any security. All data is sourced from publicly available information and believed to be accurate as of the date of publication but may be subject to change. The author may or may not hold positions in instruments mentioned. Past performance is not indicative of future results. Always conduct your own research or consult a qualified financial advisor before making investment decisions. Nothing in this publication creates a fiduciary relationship between the author and the reader.